Bangladesh has shown an impressive annual GDP growth rate of around 7% over the last decade. The economy is on track in graduating from the least developed country status in 2024 and has made impressive human development strides. PwC predicts Bangladesh to become the world’s 28th largest economy by 2030.

Micro, small, and medium enterprises (MSMEs) are the main drivers of the national economy. Contributing 25 per cent to the country’s GDP and more than 80% to employment, MSMEs play a significant role in income generation and resource utilization. The MSME consists of both producers and sellers, and both of the segments have some common and unique challenges to manage and grow the business. Lack of financial support on time is one of the common problems of MSMEs.

Around 85 percent of retailers do not maintain a ledger, and 73 percent sell on credit, according to UNCDF. This tradition is a vital reason for being excluded financially and can’t grow the business as expected. Financial exclusion leads to inadequate support from the financial institutions on time, creating a shortage in working capital, which is one of the significant barriers to growing the business.

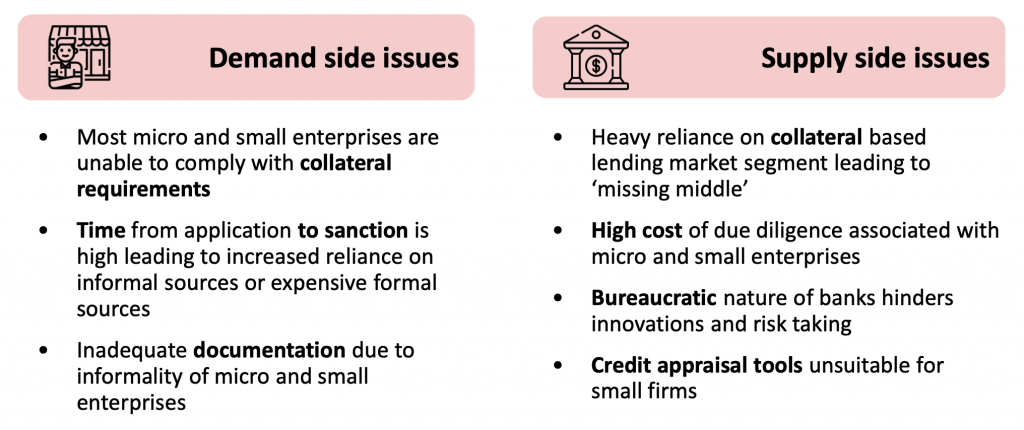

According to the economic census 2013, there are around 6.9 million micro-merchants in Bangladesh and according to the credit development forum (2016), the micro-merchants annual credit demand is US$8 billion where the credit gap is more than US$ 2 billion. There are a few fundamental gaps behind micro-merchants’ lack of adequate support from financial institutions.

There is inadequate documentation due to the traditional business management method of micro-merchants, where financial institutions have a rigorous documentation approach to get the loan. Most of the micro-merchants are unable to comply with collateral requirements. But, financial institutions are reliant on collateral-based lending. MFIs have some flexibility, but the interest rate is not favourable for micro-merchants in most cases.

Bangladesh has shown an impressive annual GDP growth rate of around 7% over the last decade. The economy is on track in graduating from the least developed country status in 2024 and has made impressive human development strides. PwC predicts Bangladesh to become the world’s 28th largest economy by 2030.

Micro, small, and medium enterprises (MSMEs) are the main drivers of the national economy. Contributing 25 per cent to the country’s GDP and more than 80% to employment, MSMEs play a significant role in income generation and resource utilization. The MSME consists of both producers and sellers, and both of the segments have some common and unique challenges to manage and grow the business. Lack of financial support on time is one of the common problems of MSMEs.

Around 85 percent of retailers do not maintain a ledger, and 73 percent sell on credit, according to UNCDF. This tradition is a vital reason for being excluded financially and can’t grow the business as expected. Financial exclusion leads to inadequate support from the financial institutions on time, creating a shortage in working capital, which is one of the significant barriers to growing the business.

According to the economic census 2013, there are around 6.9 million micro-merchants in Bangladesh and according to the credit development forum (2016), the micro-merchants annual credit demand is US$8 billion where the credit gap is more than US$ 2 billion. There are a few fundamental gaps behind micro-merchants’ lack of adequate support from financial institutions.

There is inadequate documentation due to the traditional business management method of micro-merchants, where financial institutions have a rigorous documentation approach to get the loan. Most of the micro-merchants are unable to comply with collateral requirements. But, financial institutions are reliant on collateral-based lending. MFIs have some flexibility, but the interest rate is not favourable for micro-merchants in most cases.

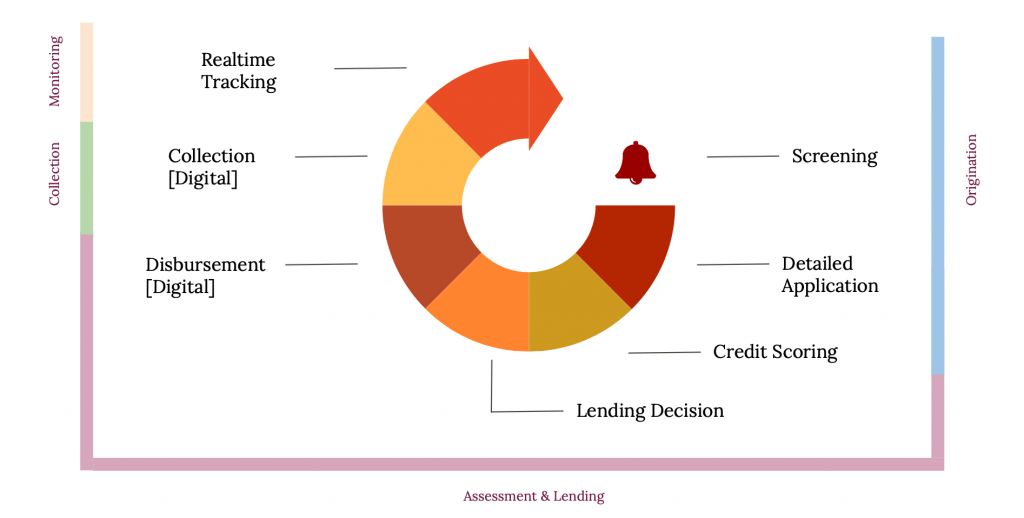

Digital and fintech platforms can minimise the mentioned gaps to democratize financial services for Micro-Merchants and the entire adult population. The significant advantage of such digitization is lowering the cost and extending convenient tools to the public. The essence of digitization is to replace the time-consuming lengthy human involved performance with technology and make the process faster and convenient.

An application that can support keeping business records digitally, provide business insights, and offer the facility to accept and pay digitally can be an ideal platform to provide data to identify the potential micro-merchants for assessing creditworthiness. In such cases, the alternative data such as digital transactions history and repayment behaviour of shop’s credit will contribute to the credit score, providing a route for access to finance to those micro-merchants who have no formal credit history in the past.

The use of alternative data is gaining popularity in many other neighbour countries like India, China, and Indonesia where innovative solutions harness the value of transaction data from bookkeeping apps, eCommerce and payment platforms, mobile phones, or even social networks as alternative sources of information to assess creditworthiness.

In Bangladesh, a few platforms are working for micro-merchant digitization like TallyKhata, which has around 3.2 million registered users, 1 million monthly active users, and 200K daily active users. This simple bookkeeping app has adequate data to create clients profiles to assess creditworthiness. There are other players in the market like sManager and Mokam by ShopUp. These platforms know their users better.

Financial institutions can be partnering with them to know more about these segments and develop products as per demands. A recent initiative from bKash and City Bank regarding introducing nano loans for bKash users is undoubtedly the beginning of a new era. The democratization of finance results from a global demand to completely rethink the financial system to make it more accessible to everyone, regardless of consumers’ living standards, income or geographic location.

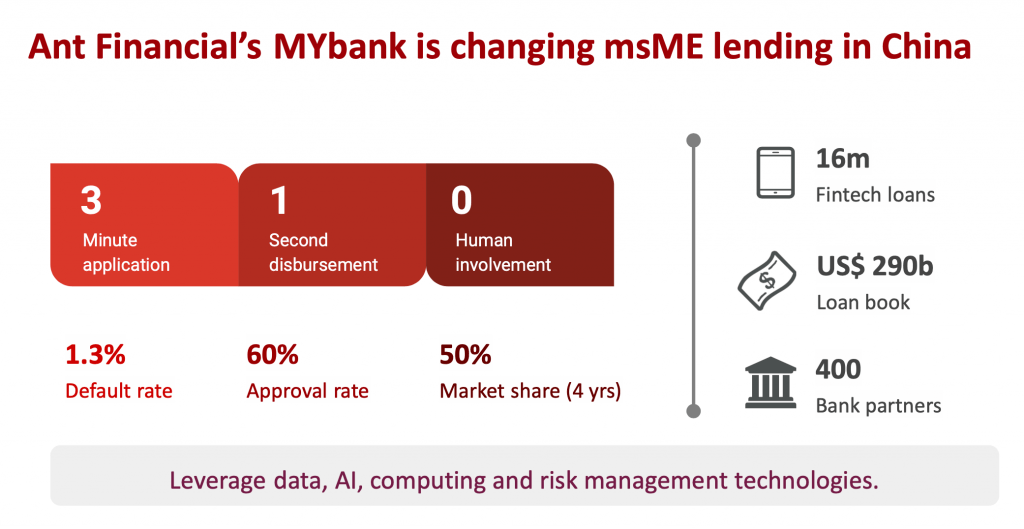

Ant Financial’s MYBank is changing China’s micro, small, and medium enterprise lending outlook. They have disbursed 16 million loans through FinTech, which is equivalent to a US$ 290 billion loan book partnering with 400 bank partners by leveraging data, AI, computing, and risk management technologies.

They have taken a 3-1-0 model; 3 minutes application, 1-second disbursement, and 0-human involvement. Their default rate is 1.3 percent, the approval rate is 60 percent, and they took 50 percent of the market share in 4 years.

Everyone should be able to participate in the coming financial services revolution. Of course, there will still need to be significant work to ensure that essential elements like risk, trust, safety, privacy and integrity of the financial system are maintained and expanded. Financial services are a highly regulated industry — as they should be.

However, if regulations don’t accommodate the technological possibilities emerging with fintech, innovative services will be hindered. This might lead to a dilemma for our policymakers to achieve the right balance between enabling innovative fintech and safeguarding the financial system. But, the policymakers should ensure this balance for the betterment of the country.

To meet the unmet demand and to ensure the financial services for all this sector needs digitisation and more innovative partnership in coming days. The democratization of financial services will have profound effects. As competition increases, traditional financial institutions must equip themselves with the best available tools and surround themselves with partners likely to make a difference to consumers.

With more information and more ability to control their economic outcomes, people will be better able to get the resources they need to prosper. Enabling sophisticated financial tools for the masses will unleash new levels of growth to lessen the scourge of poverty and all it brings with it. The key, therefore, lies in this stimulating environment, where success is synonymous with collaboration.

This article has been published in the Daily Sun on 27th December 2021

Link: https://www.daily-sun.com/printversion/details/596018/Digitisation-for-democratising-finance-to-micromerchants